Key Takeaways

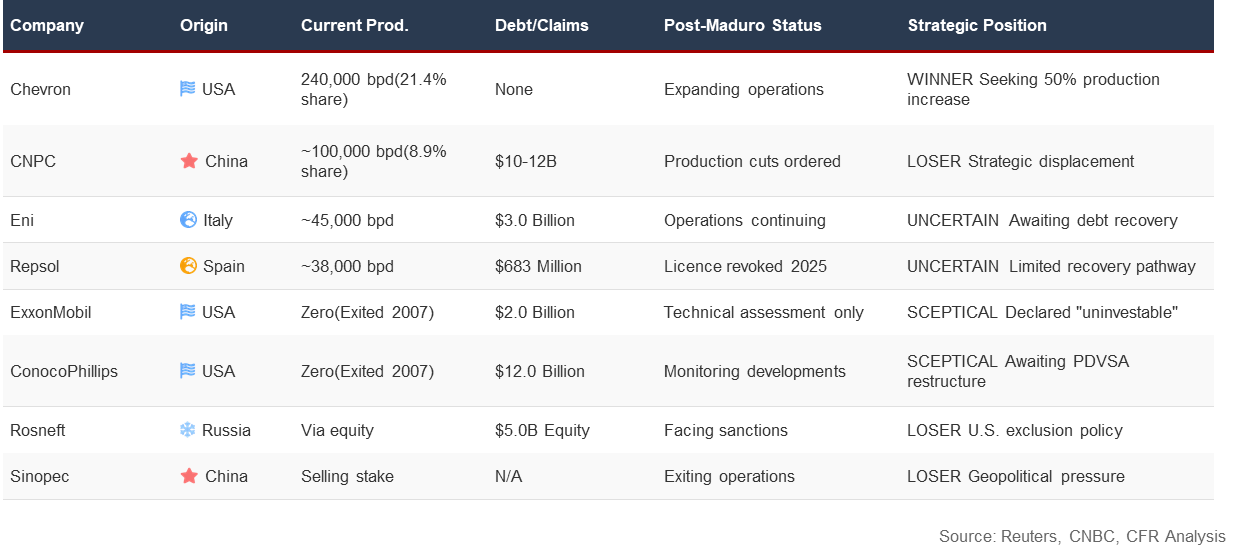

- Chevron is the sole immediate winner, positioned to increase production by 50 per cent within 18-24 months through expanded licences, whilst major IOCs like ExxonMobil and ConocoPhillips remain on the sidelines awaiting legal protections and debt resolution mechanisms.

- China faces strategic displacement, losing access to 64 per cent of Venezuelan oil exports (746,000 bpd) that it received in 2025, with Secretary of State Rubio explicitly stating the U.S. does not want China or other adversaries controlling Venezuela’s oil industry.

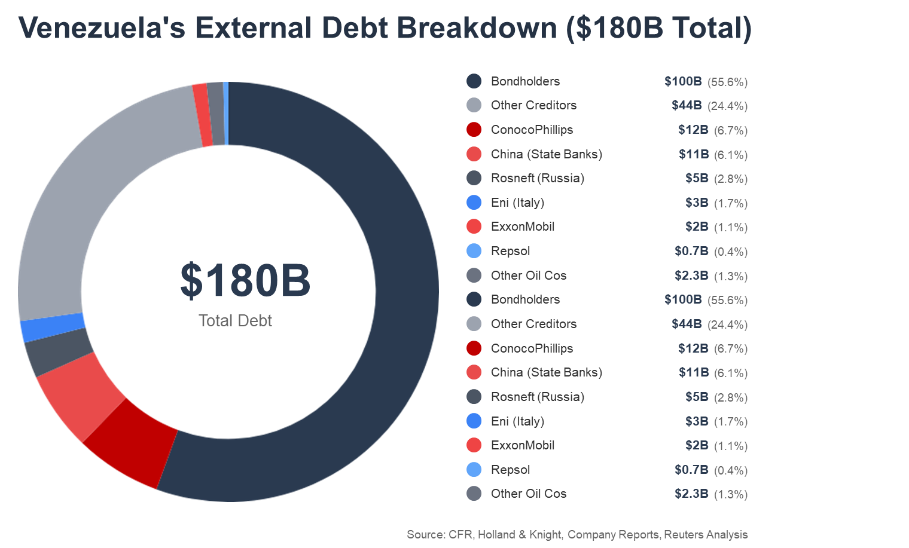

- The $150-200 billion debt overhang presents a fundamental barrier to investment, with no clear resolution pathway for $12 billion in ConocoPhillips claims, $2 billion in ExxonMobil awards, and billions owed to European creditors Eni and Repsol.

- Infrastructure reconstruction requires $10-20 billion for near-term rehabilitation and $100 billion over 10 years to return to historical production levels of 3+ million bpd, which represents a commitment far exceeding current industry appetite in a $55 per barrel price environment.

- Political instability between acting President Rodríguez and opposition leader Machado creates governance uncertainty, whilst Venezuela’s lack of bilateral investment treaties with the U.S. eliminates standard protections against expropriation that enabled the 2007 nationalisations.

Executive Summary

The U.S. military’s January 3, 2026 capture of Venezuelan President Nicolás Maduro has fundamentally altered the operating environment for international oil companies (IOCs) in Venezuela. Whilst the Trump administration has announced control over Venezuelan oil sales indefinitely and completed $500 million in initial transactions, major oil companies remain deeply sceptical about committing capital. With ExxonMobil CEO Darren Woods declaring Venezuela “uninvestable” and $150-200 billion in outstanding debt claims, the gap between policy ambition and commercial reality remains substantial.

Current Production and Infrastructure Status

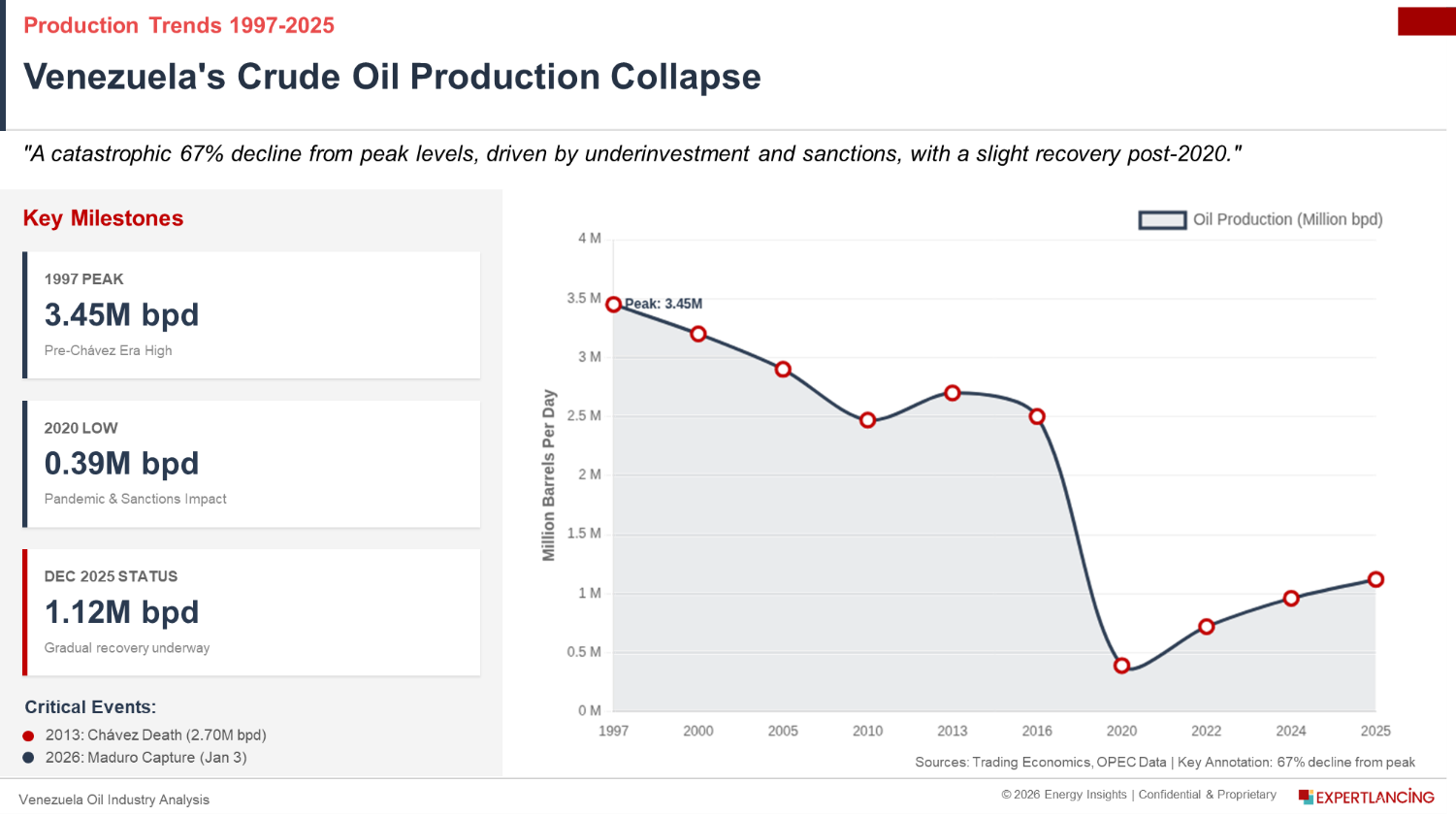

Venezuela’s oil production stands at approximately 1.12 million barrels per day (bpd) as of December 2025, representing a 67 per cent decline from the peak of 3.45 million bpd in 1997. Despite holding 303 billion barrels in proven reserves, which is the world’s largest, the country ranks only 21st globally in production.

Infrastructure decay presents the primary operational challenge. According to AP News reporting, “oil-extraction equipment and pipelines fell into disrepair and were damaged by looting during political unrest,” whilst state company PDVSA faces “deteriorating facilities, a loss of skilled workers and years of underinvestment.” The heavy, sour nature of Venezuelan crude necessitates diluents for pipeline transport and specialised refining capacity, further complicating economics in a $55 per barrel price environment.

Company Positioning: Winners, Losers, and the Uncertain

Clear Winner: Chevron Chevron emerges as the unambiguous beneficiary, currently producing approximately 240,000 bpd, which accounts for 25 per cent of Venezuela’s total output through PDVSA joint ventures. The company is expected to receive an expanded licence enabling increased production and potentially the ability to trade PDVSA’s own crude. Vice Chairman Mark Nelson indicated Chevron “can increase liftings from joint ventures 100% essentially effective immediately” and boost production “by about 50% in the next 18 to 24 months” by leveraging existing assets. Chevron shares have risen 9 per cent since Maduro’s removal.

Strategic Losers: Chinese and Russian NOCs

Chinese state-owned companies face strategic displacement. China received approximately 64 per cent of Venezuelan oil exports in 2025, amounting to roughly 746,000 bpd. However, the Trump administration’s mandate that all oil flow through “authorised channels consistent with U.S. law” effectively terminates preferential access. CNPC’s Sinovensa joint venture, which produces approximately 100,000 bpd, faces production cuts, whilst debt repayment flows allocated at 50,000-100,000 bpd against $10-12 billion owed to China have been disrupted. Secretary of State Marco Rubio explicitly stated that the U.S. “does not want China and other US adversaries to control” Venezuela’s oil industry.

Russian interests face similar exclusion. Rosneft holds approximately $5 billion in equity stakes across multiple ventures but confronts the same geopolitical headwinds under the Trump administration’s hemispheric energy dominance doctrine.

The Sceptics: ExxonMobil and ConocoPhillips

Major U.S. oil companies with historical claims remain cautious. ExxonMobil holds $984.5 million to $2 billion in arbitration awards from 2007 expropriations, whilst ConocoPhillips pursues $12 billion in claims, including an $8.7 billion ICSID award. However, President Trump dismissed these claims, stating “We’re not going to look at what people lost in the past, because that was their fault”, which fundamentally complicates the companies’ calculus. At a January 10 White House meeting, Woods told Trump that after having “assets seized there twice… to re-enter a third time would require some pretty significant changes”, emphasising the need for “durable investment protections.” ConocoPhillips CEO Ryan Lance called for “restructuring the entire Venezuelan energy system including PDVSA,” signalling deep scepticism about existing frameworks. Both companies indicated willingness to send technical assessment teams but declined capital commitments.

European Creditors in Limbo

Italian energy company Eni is owed $2.3-3 billion as of end-2025, whilst Spanish firm Repsol claims €586 million, equivalent to $683 million. Both continue gas production operations but lack clear debt recovery mechanisms after the U.S. revoked Repsol’s licence for oil-for-debt arrangements in March 2025.

The Investment Barrier: Capital, Debt, and Legal Frameworks

Reconstruction economics present a fundamental challenge. Council on Foreign Relations analysis estimates that $10-20 billion is required for near-term rehabilitation of existing fields, with a 2-3 year timeline to reach 1.5 million bpd. Meanwhile, returning to 3+ million bpd would require $100 billion over 10 years. Alternative industry estimates reach $183 billion over 15 years. For context, ExxonMobil’s entire 2026 global capital budget is approximately $28 billion, which means Trump’s $100 billion Venezuela target is equivalent to 3.5 years of Exxon’s worldwide spending. The debt overhang compounds capital constraints significantly. Venezuela’s total external debt is estimated at $150-200 billion, which includes $100 billion to bondholders, $10-12 billion to China, $5 billion to Russia, and $15-17 billion in oil company arbitration awards. Holland & Knight legal analysis identifies a critical gap. Venezuela lacks bilateral investment treaties (BITs) or free trade agreements with investment chapters with the U.S., thereby eliminating standard protections against expropriation or international arbitration access. Without these frameworks, companies face the same legal vacuum that enabled the 2007 nationalisations.

Political Risk: The Rodríguez-Machado Dynamic

Political uncertainty compounds commercial risks substantially. Acting President Delcy Rodríguez, who was Maduro’s former vice president and was sworn in on January 5, competes with opposition leader María Corina Machado, the 2025 Nobel Peace Prize laureate, for control of Venezuela’s future and Trump’s favour. According to CFR’s Will Freeman, Rodríguez must “convince the Trump administration that she is working with them… but also… convince hardliners in the Maduro regime… that she’s not going to sell them out.” This represents a precarious tightrope walk that is unlikely to provide the durable stability that major IOCs require for billion-dollar commitments.